ECB Stress Test Results 2023

In 2023, the ECB Banking Supervision conducted two separate stress test exercises involving euro area's significant institutions. A total of 57 institutions were directly supervised in the EU-wide test coordinated with other financial authorities like the European Banking Authority (EBA), while 41 additional significant institutions were part of a parallel stress test overseen by the ECB. The results published on the 28th July 2023, can be found here.

The stress tests were designed to evaluate the ability of banks to handle financial and economic shocks. Using 2022 year-end data, the tests analysed how each bank's capital position would change over a three-year period under both standard and adverse conditions. The exercises supplied a unified framework to gauge the resilience of the banks to specific shocks, such as an extended period of low growth and high inflation.

Unique to the 2023 adverse scenario were concerns over escalating geopolitical tensions leading to stagflation and increased interest rates. This was markedly different from the 2021 adverse scenario, which had assumed falling interest rates. Overall, the stress test results affirmed that the euro area banking sector could withstand severe economic downturns. The system-level CET1 ratio, a key measure of bank solvency, revealed a depletion but remained at acceptable levels in the adverse scenario.

However, the results were heterogeneous across banks, reflecting the diverse business models and balance sheet structures. Restrictions on dividend payments were applied to some banks during the projection horizon, but only a small number would struggle to meet legal capital requirements. Still, no immediate recapitalization actions were required

Key factors driving depletion included credit and market risk losses, costs linked to funding, and rising administrative expenses due to inflationary pressures. Improved asset quality and banks' enhanced income-generating capacity, owing to an expansion of lending margins and rising interest rates in the past year, made them more resilient to the adverse scenario compared to the previous year's stress test.

There were also some qualitative findings, particularly around risk data aggregation issues (ECB is currently finalising its guidance to Banks regarding RADRR - Guide on effective risk data aggregation and risk reporting) and deficiencies in new elements of the stress test, such as credit risk modelling. The results will inform ongoing supervisory dialogues and will impact Pillar 2 requirements and guidance, serving to strengthen market discipline.

Overall, the 2023 stress tests indicate a slightly improved resilience of the banking sector, owing to positive trends in asset quality and the banks' ability to generate income. The exercise emphasizes the importance of these periodic tests as part of the larger risk management strategy, while also highlighting the need for individual banks to conduct their own assessments tailored to their unique risk profiles.

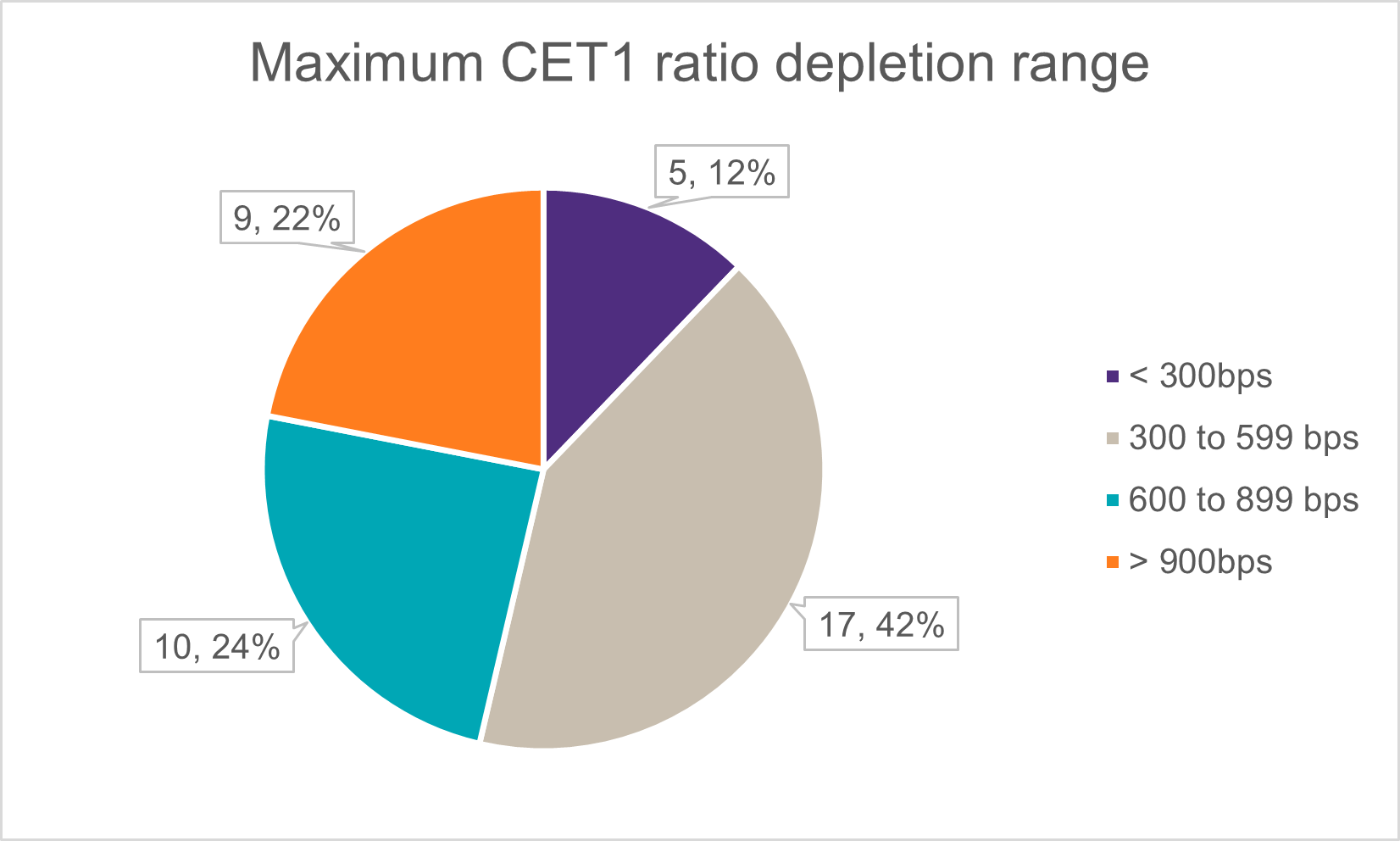

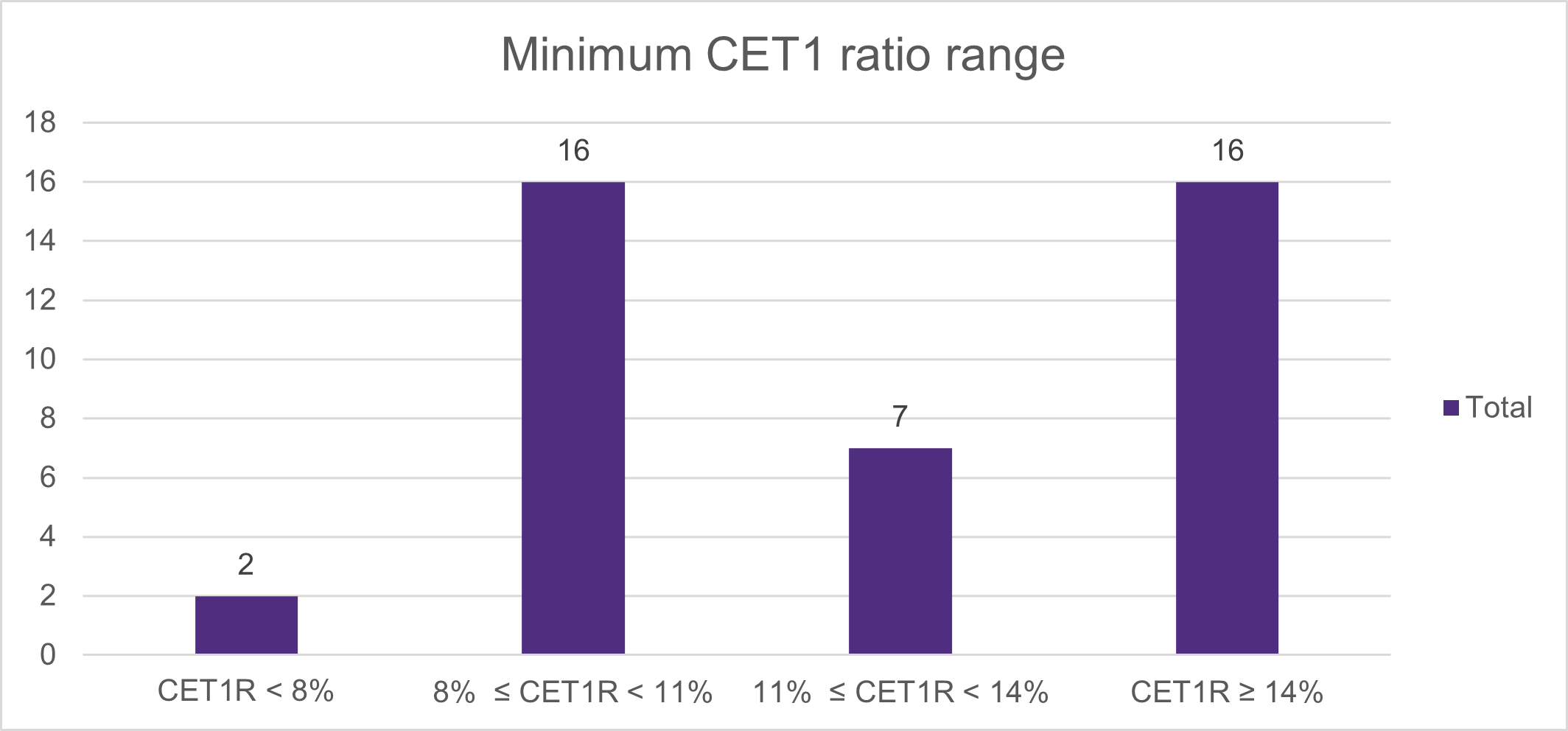

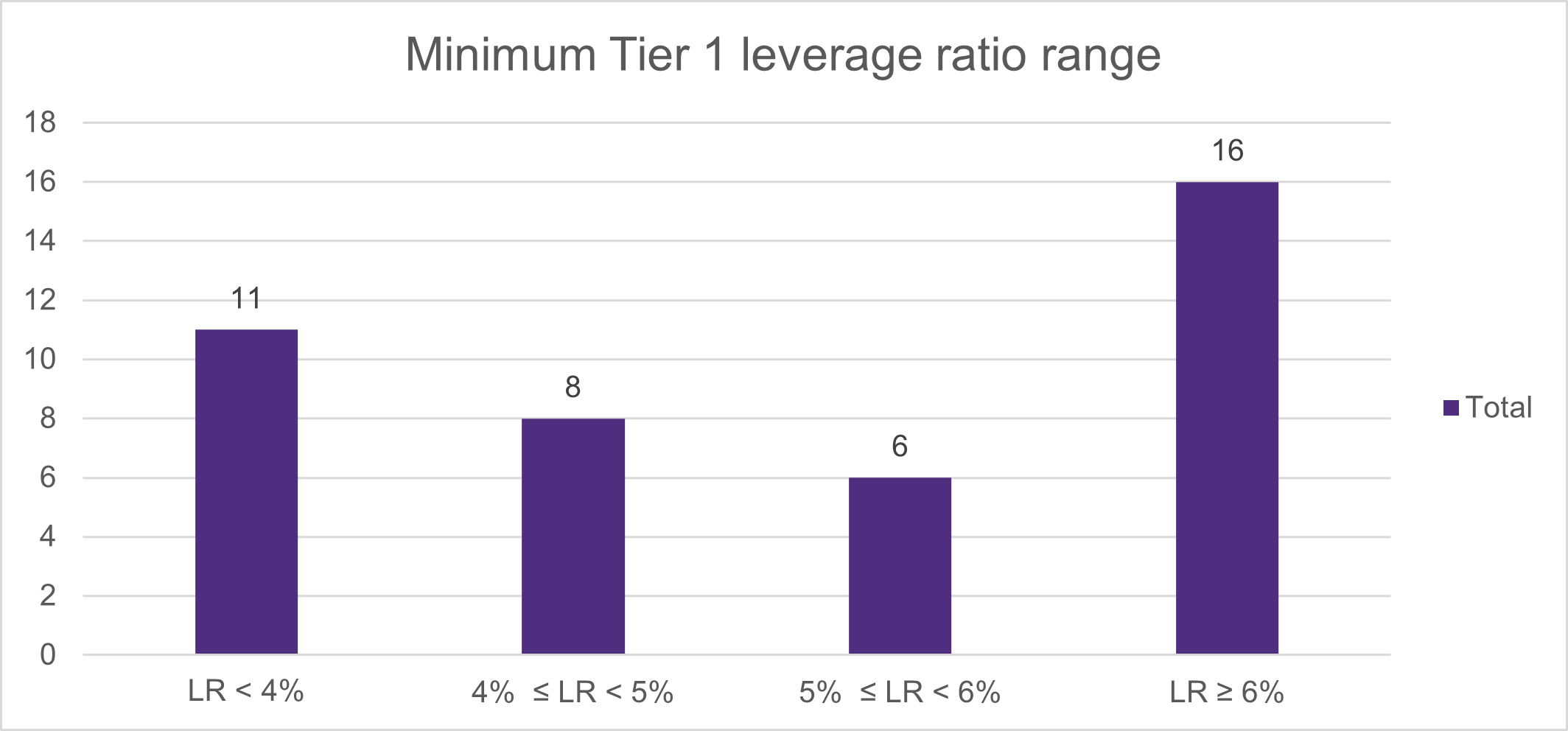

Bank of Cyprus and Hellenic Bank were among the further 41 significant institutions directly supervised by the ECB took part in the parallel stress test coordinated by the ECB. For the Cyprus Banks, the results are shown below. Bank of Cyprus ranks in the 300 to 599 bps CET1 ratio depletion range with a minimum CET1 ratio in the range 8% to 11%, while Hellenic Bank ranks in the 600 to 899 bps of depletion with a minimum CET1 ratio in the range 11% to 14%.

|

|

High-level individual results by range |

Scenario sensitivities: 2023-2025 projections |

|

|||||

|

Institution |

Sample |

Maximum CET1 ratio (FL) depletion by ranges |

Minimum CET1 ratio (FL) by ranges |

Minimum Tier 1 leverage ratio (FL) by ranges |

Delta projected NII adverse vs. baseline scenario (in %) |

Delta projected LLPs adverse vs. baseline scenario (in %)1 |

Delta projected profit/ loss adverse vs. base-line scenario (in %) |

|

|

Bank of Cyprus Holdings Public Limited Company |

SSM |

300 to 599 bps |

8% ≤ CET1R < 11% |

5% ≤ LR < 6% |

-3.7% |

4.4% |

-9.0% |

|

|

Hellenic Bank Public Company Limited |

SSM |

600 to 899 bps |

11% ≤ CET1R < 14% |

LR < 4% |

-7.6% |

4.2% |

-10.0% |

|

From the sample of 41 significant institutions directly supervised by the ECB, below we present the distribution of CET1 Ration Depletion ranges.

The below figure shows the distribution to Minimum CET 1 ratio range. Bank of Cyprus falls under the 8% to 11% range, while Hellenic Bank CET1 Ratio drops to a higher range of 11% to 14% under the adverse scenario.

The below figure shows the distribution to Minimum Tier 1 leverage ratio range. Bank of Cyprus falls under the 5% to 6%range, while Hellenic Bank CET1 Ratio drops less than 4% under the adverse scenario.

Article by,

Phanis Ioannou, Manager, Quantitative Risk Services